CRU deductions: what claimants in Scotland must know

TL;DR:

- Many claimants mistakenly believe full compensation lands in their account after a successful injury claim, but the CRU recovers benefits and NHS costs before you receive your payout. The CRU, part of the DWP, ensures the state is reimbursed for benefits or treatments paid due to an accident, preventing double recovery and deducting these amounts from your settlement. Proper early understanding and legal guidance on CRU deductions can significantly improve your net compensation and prevent surprises at settlement.

Many Scots assume that once a personal injury claim succeeds, the full compensation amount lands in their account. That assumption is wrong, and it catches people off guard every year. In UK personal injury and clinical negligence cases, the Department for Work and Pensions operates the Compensation Recovery Unit (CRU), which works with insurers and solicitors to recover certain state benefits and NHS treatment costs from the responsible party’s insurer after a compensation payment is made. Understanding how this works before you settle can protect your final payout.

Table of Contents

Key Takeaways

| Point |

Details |

| CRU reduces double recovery |

The Compensation Recovery Unit ensures you do not receive both state benefits and compensation for the same loss. |

| Benefits and NHS costs are deducted |

Relevant state benefits and certain NHS injury charges are deducted before final compensation is paid out. |

| Solicitors handle CRU communications |

Your solicitor normally manages all contact with the CRU, ensuring proper paperwork and deductions. |

| Check your CRU certificate |

Ask to confirm your CRU certificate to avoid surprises when your case settles. |

Understanding the role of the Compensation Recovery Unit

The Compensation Recovery Unit is a branch of the Department for Work and Pensions (DWP). Its core job is straightforward: make sure the state is reimbursed for money it has already spent on you because of your injury. If you received benefits or NHS treatment as a direct result of an accident, the state covered those costs. When you then receive compensation from the at-fault party, the CRU steps in to reclaim that expenditure from the insurer.

The principle behind this is called preventing “double recovery.” You cannot receive compensation for a loss that the state has already covered. Without the CRU, a claimant could effectively be paid twice for the same loss: once through state benefits and again through compensation. The CRU closes that gap.

Here is what the CRU specifically recovers:

- Social security benefits paid to you because of the accident, injury, or disease

- NHS hospital costs incurred in treating injuries from road traffic accidents and personal injury claims

- NHS ambulance trust charges for emergency responses linked to qualifying accidents

“CRU recovers amounts of social security benefits paid due to an accident, injury, or disease under the Compensation Recovery Scheme, and costs incurred by NHS hospitals and ambulance trusts for treatment.”

It is worth noting that the CRU does not take money from you directly. The recovery comes from the compensating party, typically the defendant’s insurer, before the final settlement figure reaches you. Understanding this distinction helps you see how your compensation payout in Scotland is calculated and why the headline figure in negotiations may differ from what you ultimately receive.

How the CRU affects your Scottish personal injury claim

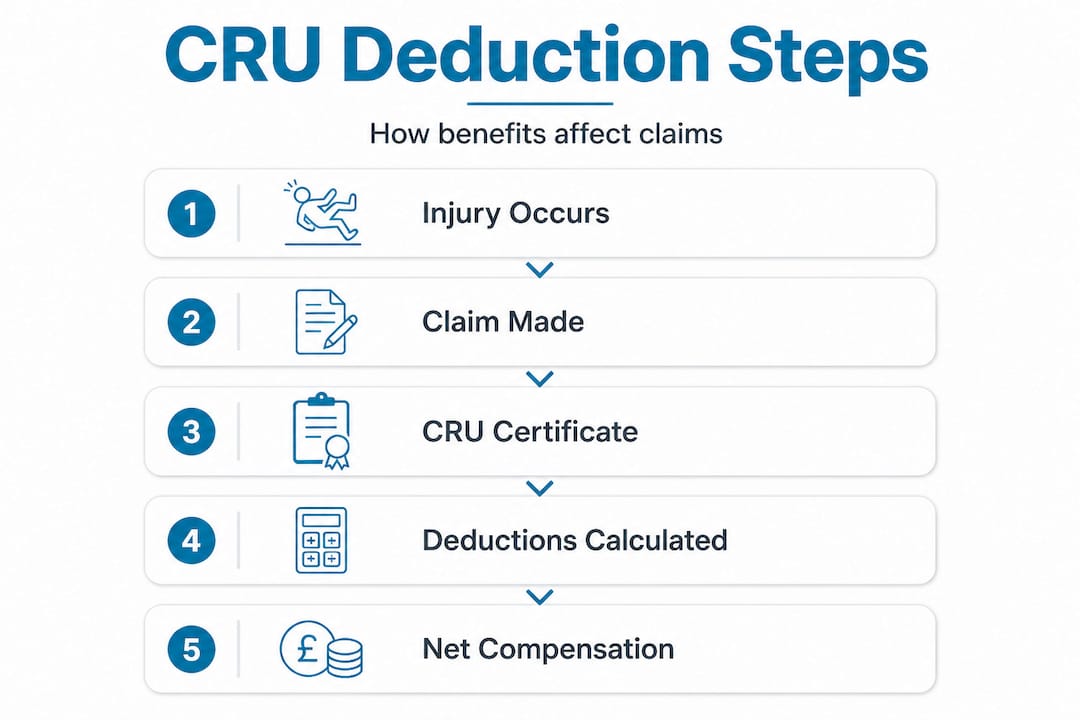

With the CRU’s role established, it is vital to understand how its actions directly influence your claim outcome. The process is not random. It follows a defined sequence, and knowing each stage helps you anticipate where deductions might arise.

Here is how the CRU interacts with your claim from start to finish:

- Notification. As soon as a personal injury claim is made, the compensator (usually the insurer) must notify the CRU. This is a legal obligation, not optional.

- Certificate of recoverable benefits. The CRU issues a certificate listing every recoverable benefit paid to you since the date of your accident. This document sets out the exact sums the insurer must repay to the state.

- Assessment period. The recovery period typically runs from the date of the accident up to the date of settlement, or for a maximum of five years, whichever comes first.

- Deduction from the award. The insurer pays the CRU directly. The recoverable benefits are offset against specific heads of damage in your claim, such as loss of earnings or care costs.

- Final payment to you. Only after the CRU has been satisfied does the remaining compensation reach you.

The specific benefits the CRU can recover include Employment and Support Allowance (ESA), Jobseeker’s Allowance (JSA), and other qualifying payments. The calculation of compensation must therefore account for these deductions from the outset, not as an afterthought at the end of the process.

Pro Tip: Ask your solicitor to request the CRU certificate early in your claim. Knowing the recoverable amount in advance allows you and your legal team to negotiate a settlement that still leaves you with a fair net figure. Many claimants who follow a step-by-step claim guide find that early transparency about CRU figures avoids last-minute surprises.

One critical point: the recoverable benefits are offset against comparable heads of damage only. For example, ESA can only be deducted from a compensation award for loss of earnings, not from the pain and suffering element of your claim. This matching rule is important because it protects part of your award from CRU recovery. A good solicitor will structure your claim to maximise the portions of compensation that are not subject to offset.

What benefit types and NHS charges are recovered?

Understanding which payments the CRU can recover is crucial when estimating your potential net compensation. Not every benefit you have ever received is fair game. The CRU only recovers payments that are directly linked to the injury or accident in question.

| Recoverable benefits |

Recoverable NHS costs |

| Employment and Support Allowance (ESA) |

NHS hospital treatment (injury-related) |

| Jobseeker’s Allowance (JSA) |

NHS ambulance charges (qualifying accidents) |

| Disability Living Allowance (DLA) |

A&E attendance following the accident |

| Income Support |

Inpatient and outpatient treatment |

| Carer’s Allowance |

Surgical procedures related to the injury |

| Universal Credit (injury-related element) |

Physiotherapy on NHS referral |

| Incapacity Benefit |

Specialist consultations (NHS) |

The CRU recovers NHS charges from liable parties in personal injury claims, but only for treatment that is directly connected to the injury being claimed for. If you had an unrelated hospital admission during the same period, those costs are not recoverable.

What is not recovered:

- Benefits you were already receiving before the accident for unrelated conditions

- NHS treatment for pre-existing conditions that the accident did not worsen

- Private medical costs (these are handled differently within the compensation claim itself)

- Benefits paid more than five years after the accident date

This distinction matters enormously. If you have a long-term disability that predates your accident, the benefits paid for that condition are ring-fenced. The CRU can only pursue what it can prove was paid because of the injury being claimed for. Keeping clear medical records that separate pre-existing conditions from accident-related ones is therefore genuinely useful.

Understanding the full range of compensation types in Scotland helps you see how CRU deductions interact with each head of damage. It also reinforces why acting within the claim process deadlines matters: delays can extend the period over which benefits accrue, potentially increasing the recoverable sum.

Important callout: The five-year cap on the CRU recovery period means that claimants with long-term injuries who settle quickly may face lower deductions than those who wait. Timing your settlement strategically, with proper legal advice, can make a real financial difference.

Communicating with the CRU during your claim

Now that you appreciate what is deducted, it is important to know how the CRU process works in practice, including how to handle questions or potential issues. The good news for most claimants is that you will rarely need to contact the CRU yourself.

Here is how communication with the CRU typically flows during a Scottish personal injury claim:

- Your solicitor notifies the CRU on your behalf when the claim begins. This triggers the certificate process.

- The insurer liaises with the CRU to obtain the certificate of recoverable benefits and confirm the amounts owed.

- Your solicitor reviews the certificate to check it is accurate and to structure the claim accordingly.

- Settlement negotiations proceed with the CRU figures factored in. Your solicitor ensures the deductions are applied to the correct heads of damage.

- The insurer pays the CRU directly at settlement. You receive the net figure after this payment.

The official contact routing for the CRU is via GOV.UK guidance, which directs claim-related contact through specific phone and email channels depending on the nature of the query. There are different contact routes for benefit recovery queries versus NHS cost recovery queries, so it is important to use the correct channel if you do need to raise an issue.

Pro Tip: If you believe the CRU certificate contains an error, do not wait until settlement to raise it. Errors in the certificate can be challenged through a formal dispute process, but this takes time. Raising concerns early, through your solicitor, gives you the best chance of resolving discrepancies before they affect your payout.

Effective injury compensation management involves treating the CRU certificate as a live document throughout your claim, not a formality to deal with at the end. If your benefit entitlements change during the claim, the certificate may need to be updated. Your solicitor should monitor this actively. You can also use a compensation calculator to get a rough sense of your potential award before factoring in CRU deductions, which helps set realistic expectations.

What most claimants (and even many solicitors) overlook about CRU deductions

Armed with knowledge of CRU processes and communications, let us examine what most people, and even some legal advisers, miss about how these deductions really play out.

The most common blind spot is timing. Claimants often focus on the gross compensation figure during negotiations and only discover the CRU deduction at the point of settlement. By then, there is very little room to manoeuvre. The insurer has already paid the CRU, and the claimant receives whatever is left. This is not a theoretical risk. It happens regularly, particularly in claims that take two or three years to resolve, during which time benefit payments accumulate quietly in the background.

The second overlooked issue is NHS cost recovery. Many solicitors are highly familiar with benefit deductions but pay less attention to NHS charges, which can include multiple hospital admissions, ambulance callouts, and extended physiotherapy. In serious injury cases, these costs can run into thousands of pounds. The CRU ensures claimants cannot recover the same loss twice, but the deductions can be complex and surprise many individuals, particularly when NHS costs are higher than anticipated.

There is also a structural problem in how some claims are settled. If a solicitor does not carefully allocate the compensation award across the correct heads of damage, the CRU may end up offsetting benefits against the pain and suffering element of the award, which should be protected. This is technically incorrect, but it can happen when paperwork is rushed or the certificate is not scrutinised properly.

Our view, based on the pattern we see in claim examples in Scotland, is that claimants who engage solicitors with specific CRU experience consistently achieve better net outcomes than those who treat CRU as an administrative afterthought. The difference is not always dramatic, but on a claim worth £30,000 or more, even a £2,000 to £3,000 improvement in how deductions are structured is significant.

Keep records of every benefit you receive from the date of your accident. Note the dates, amounts, and the stated reason for each payment. If the CRU certificate later lists a benefit you believe is unrelated to your injury, you have the evidence to challenge it. This is simple, costs nothing, and is the kind of preparation that separates claimants who are surprised at settlement from those who are not.

Free expert support for CRU and personal injury claims

If CRU deductions or the injury claim process seem overwhelming, you do not have to go it alone. At Scotland Claims, we connect injured people across Scotland with specialist solicitors who understand the CRU process inside out. Our No Win No Fee guidance means you pay nothing upfront and nothing at all if your claim is unsuccessful. Our network of injury lawyers in Scotland will handle all CRU communications, review certificates for accuracy, and structure your claim to protect as much of your award as possible. Start with our free personal injury compensation calculator to get an initial estimate, then request a callback for tailored advice with no obligation.

Frequently asked questions

Will CRU deductions always reduce my compensation payout?

Only if you have received qualifying state benefits or NHS injury treatment linked to your accident. If you received no such benefits, the CRU recovers nothing and your payout is unaffected.

Can I dispute the amount the CRU wants to recover?

Yes, there is a formal appeals process if you believe the certificate is incorrect. The official CRU contact routing via GOV.UK directs you to the correct channel for raising disputes, and your solicitor should handle this on your behalf.

What happens if my solicitor fails to check CRU deductions?

You may face an unexpectedly lower final payout. Always confirm the CRU certificate has been reviewed before agreeing settlement terms, as deduction errors can impact your final settlement figure significantly.

Are all NHS costs recoverable via the CRU?

No. Only NHS treatment costs from road traffic and personal injury claims are recoverable. Unrelated NHS treatment, or treatment for pre-existing conditions, is not included.

Usually not. Your solicitor or insurer manages all CRU communications. If you need to check details yourself, the GOV.UK guidance page lists the correct contact channels by claim type.

Recommended