What is legal expenses insurance? A guide for Scotland

TL;DR:

- Legal expenses insurance (LEI) covers legal costs for unexpected disputes, including personal injury claims, when purchased as an add-on to home or motor policies. It provides proactive legal support, but only if claimants meet specific prospects tests and notify insurers promptly, especially in Scotland. Understanding LEI’s scope and limits ensures claimants access justice without unexpected costs or delays.

Legal expenses insurance (LEI) is a type of cover that pays for your legal costs when you face an unexpected dispute, including personal injury claims. Known formally as “before-the-event” insurance, LEI is typically available as an add-on to home or motor insurance policies for as little as £30 per year, with coverage limits ranging from £25,000 to £100,000. For individuals in Scotland pursuing personal injury compensation, understanding what LEI covers, how it works in practice, and where its limits lie can make the difference between pursuing a legitimate claim and walking away from one.

What is legal expenses insurance and what does it cover?

Legal expenses insurance is defined as a policy that funds the cost of legal representation and, where relevant, your opponent’s legal costs if your claim is unsuccessful. The Law Society confirms that most LEI policies also include access to a 24-hour legal advice helpline, which can resolve many disputes without formal legal action ever being needed. That helpline access alone is worth the annual premium for many policyholders.

The scope of a standard LEI policy typically covers the following situations:

- Personal injury claims arising from road traffic accidents, workplace accidents, and slips or trips

- Property disputes with neighbours or landlords

- Consumer disputes involving faulty goods or services

- Employment issues such as unfair dismissal or discrimination

Common exclusions are equally important to understand. Home insurance legal cover typically excludes family law matters, disputes with a value under £250, and any legal issue that arose before the policy start date. These exclusions catch many claimants off guard, particularly those who assume their existing home or motor policy already covers them in full.

Pro Tip: Check your existing home and motor insurance documents before purchasing a standalone LEI policy. Many people already have a basic level of legal cover attached to policies they hold, though the scope is often narrower than a dedicated LEI product.

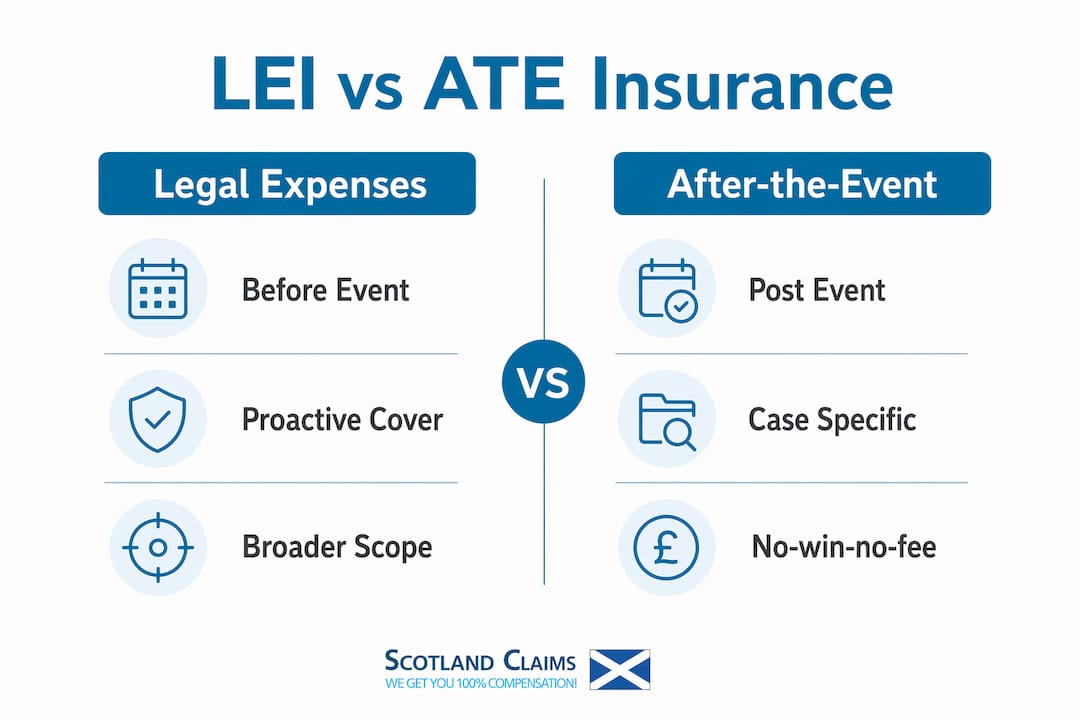

How does legal expenses insurance differ from after-the-event insurance?

The distinction between LEI and after-the-event (ATE) insurance is one of timing and purpose. LEI is proactive cover purchased before any legal dispute arises, whereas ATE insurance is bought after a dispute has already begun, specifically to cover the risk of losing a case that is already in progress.

The table below sets out the core differences between the two types of legal expense protection:

| Feature |

Legal expenses insurance (LEI) |

After-the-event insurance (ATE) |

| When purchased |

Before any dispute arises |

After a dispute or accident has occurred |

| Primary purpose |

Proactive cover for unexpected legal issues |

Secondary protection during active litigation |

| Typical cost |

Around £30 per year as an add-on |

Variable; often a percentage of the claim value |

| Common use |

Personal injury, property, employment disputes |

No-win-no-fee personal injury litigation |

| Covers opponent’s costs |

Yes, if claim is unsuccessful |

Yes, typically the core purpose of ATE |

ATE insurance is frequently used alongside no-win-no-fee agreements in personal injury cases. If a solicitor takes on a case under a conditional fee arrangement and the claim fails, ATE covers the opponent’s legal costs so the claimant faces no financial liability. For Scottish claimants, this means ATE and LEI can both be relevant at different stages of the same claim. LEI may fund early legal advice and representation, while ATE steps in as a safety net if formal court proceedings follow.

What Scottish claimants need to know about using LEI in personal injury cases

Using LEI for a personal injury claim in Scotland involves several practical steps that many claimants overlook. The most critical is timing. Insurers require early notification of any potential claim, and any legal costs incurred before the insurer appoints a solicitor are generally not covered. This means contacting your insurer as soon as possible after an accident, not weeks later when you have already instructed a lawyer independently.

Key practical points for Scottish claimants include:

- The 51% rule: Insurers will only fund legal representation if an independent lawyer assesses there is more than a 51% chance of success. This is known as the “reasonable prospects of success” test.

- Panel solicitors: LEI providers typically require you to use solicitors from their approved panel to control costs. You can choose your own solicitor once formal court proceedings begin, but only up to the insurer’s rate. You pay any difference above that rate yourself.

- Second opinions: If your insurer rejects your claim on the basis of insufficient prospects, you can obtain a second legal opinion at your own cost. If that opinion supports your case, the cost may be reimbursed.

- Coverage limits apply: Even within a valid claim, the policy limit (often between £25,000 and £100,000) caps total expenditure. Complex litigation can exceed these limits.

- No retrospective cover: LEI only applies to events that occur after the policy start date. An accident that predates your policy is not covered regardless of when you make the claim.

Understanding expert assessment in claims is particularly relevant here, as LEI may fund the cost of expert medical or technical evidence that strengthens your case and satisfies the insurer’s prospects test.

Pro Tip: Notify your LEI insurer on the same day as the accident if possible. The earlier you engage them, the more of your legal costs fall within the covered period. Delayed notification is one of the most common reasons valid claims are partially rejected.

What are the benefits and limitations of LEI for personal injury claimants?

The primary benefit of legal expenses cover is access to justice. LEI removes the financial barriers that prevent individuals from pursuing legitimate claims, particularly those who cannot afford solicitor fees upfront. For someone injured in a road traffic accident or a workplace incident in Scotland, knowing that legal costs are covered removes one of the most significant sources of anxiety during an already difficult period.

The benefits extend beyond cost coverage alone. The 24-hour legal helpline included in most policies provides immediate guidance on whether a claim is worth pursuing, what evidence to gather, and what timescales apply. This early advice frequently shapes the strength of a claim before formal proceedings begin.

That said, LEI has real limitations that claimants must understand before relying on it:

- Policies contain strict coverage triggers. A claim that does not meet the insurer’s prospects test receives no funding regardless of how genuine the injury is.

- Sub-limits within policies may cap specific types of costs, such as expert witness fees, at amounts lower than the overall policy limit.

- Insurer discretion plays a significant role. The insurer, not the claimant, decides whether to fund representation and which solicitor to appoint.

- LEI is almost always an extra purchase and not included automatically in standard home or motor insurance. Many people discover this only when they try to make a claim.

“Many claimants do not realise LEI requires insurer approval before legal work begins. Unapproved costs may be rejected, which makes early notification critical.” — The Law Society

Before relying on LEI for a personal injury claim, verify three things in your policy: the coverage limit, the list of covered events, and the notification requirements. These three factors determine whether your policy will actually support you when you need it.

Key takeaways

Legal expenses insurance is most valuable when claimants understand its terms before an accident occurs, not after.

| Point |

Details |

| LEI is before-the-event cover |

It must be purchased before a dispute arises; it does not cover pre-existing legal issues. |

| The 51% rule is the gateway |

Insurers only fund representation when an independent lawyer confirms more than a 51% chance of success. |

| Early notification is non-negotiable |

Costs incurred before the insurer appoints a solicitor are typically excluded from cover. |

| LEI is rarely automatic |

It is almost always a separate add-on to home or motor insurance, not included by default. |

| ATE insurance fills the gap |

After-the-event insurance provides secondary protection in active litigation when LEI is not in place. |

Why LEI matters more than most claimants realise

Roger here. After years of working with personal injury claimants across Scotland, the single most consistent mistake I see is people discovering what their LEI policy does not cover at the worst possible moment. They assumed their home insurance included full legal protection. It did not. They instructed a solicitor before notifying their insurer. Those costs were rejected. These are not edge cases. They happen regularly.

The uncomfortable truth about LEI is that its value is entirely dependent on how well you understand it before you need it. A £30 annual premium is genuinely good value for the protection it offers, but only if you read the policy, know the exclusions, and contact your insurer immediately after an incident. The claimants who benefit most from LEI are those who treat it as an active tool rather than a passive safety net.

One thing I would add specifically for those in Scotland: the solicitor fee structure here is already more favourable than in England and Wales. For serious injuries such as workplace accidents or slips and trips, Scottish solicitor fees are among the most competitive available, with Scotland Claims Injury Lawyers charging no success fee deduction at all on any claim type. That context matters when weighing up whether LEI or a no-win-no-fee arrangement better suits your situation. Sometimes the answer is both, used at different stages of the same claim.

— Roger

How Scotland Claims Injury Lawyers can support your personal injury claim

If you have been injured in Scotland and are weighing up your legal options, Scotland Claims Injury Lawyers connects you with specialist injury lawyers who understand both LEI and no-win-no-fee arrangements. For road traffic accident injuries where you are not at fault, you keep 100% of your compensation. For all claim types including workplace accidents and slips or trips, Scotland Claims Injury Lawyers deducts no success fee whatsoever, meaning you keep 100% of your compensation - while most other large firms charge up to 20% including VAT. Explore your no win no fee options or use the compensation calculator to estimate what your claim could be worth. Speak to injury lawyers in Scotland today with no upfront cost and no financial risk.

FAQ

What is legal expenses insurance in simple terms?

Legal expenses insurance is a type of cover that pays your legal costs if you face an unexpected dispute, such as a personal injury claim. It is typically purchased as an add-on to home or motor insurance for around £30 per year.

Does my home or car insurance automatically include legal cover?

No. LEI is almost always a separate add-on and not included automatically in standard home or motor insurance policies. Check your policy documents carefully to confirm whether legal cover is included.

What happens if my insurer says my case has no reasonable prospects?

If your insurer rejects your claim on prospects grounds, you can obtain a second legal opinion at your own cost. If that opinion supports your case’s viability, the cost of the second opinion may be reimbursed by the insurer.

Can I choose my own solicitor with legal expenses insurance?

You can generally choose your own solicitor once formal court proceedings begin, but only up to the insurer’s approved rate. Any fees above that rate are your responsibility to cover.

How does LEI interact with no-win-no-fee personal injury claims in Scotland?

LEI can fund early legal advice and representation before formal proceedings begin, while a no-win-no-fee arrangement covers the litigation phase. Understanding personal injury rights in Scotland helps claimants decide which funding route, or combination of routes, best suits their circumstances.

Recommended