What are share options: a guide for employees in Scotland

TL;DR:

- Share options are contractual rights allowing employees to buy company shares at a fixed price in the future without immediate ownership. The scheme type determines their tax efficiency, with EMI and CSOP offering significant tax advantages, especially in Scotland’s high 48% tax environment. Proper understanding of vesting, exercise conditions, and reporting obligations helps employees maximize options’ value and avoid costly surprises.

Share options are defined as contractual rights that give you the legal right to buy a set number of company shares at a fixed price on a future date. They are not immediate share ownership. You pay nothing upfront, and in most tax-advantaged schemes, you face no tax at the point of grant. For employees in Scotland, understanding share options matters because Scottish income tax rates reach up to 48%, making the choice of scheme type a significant financial decision. This guide covers the main types, how they work in practice, and what the 2026 tax rules mean for you.

What are share options and how do they differ from direct shares?

A share option is a right, not an obligation. You can choose to exercise it or let it lapse. This is the key distinction from a direct share award, where shares transfer immediately to your ownership with immediate tax consequences.

With a direct share award, you become a shareholder on day one. With a share option, you hold a contractual promise. You only become a shareholder once you exercise the option and pay the agreed exercise price. Until that point, you have no voting rights and receive no dividends.

The exercise price is typically set at the market value of the shares on the date the option is granted. Some schemes set it lower, or even at nil value, which increases the financial gain on exercise but also increases the tax exposure in non-tax-advantaged schemes.

Share options are most commonly used by growth companies and start-ups to attract and retain talent without paying higher salaries. They align your financial interests with the company’s performance, which is why they are popular across the UK tech and professional services sectors.

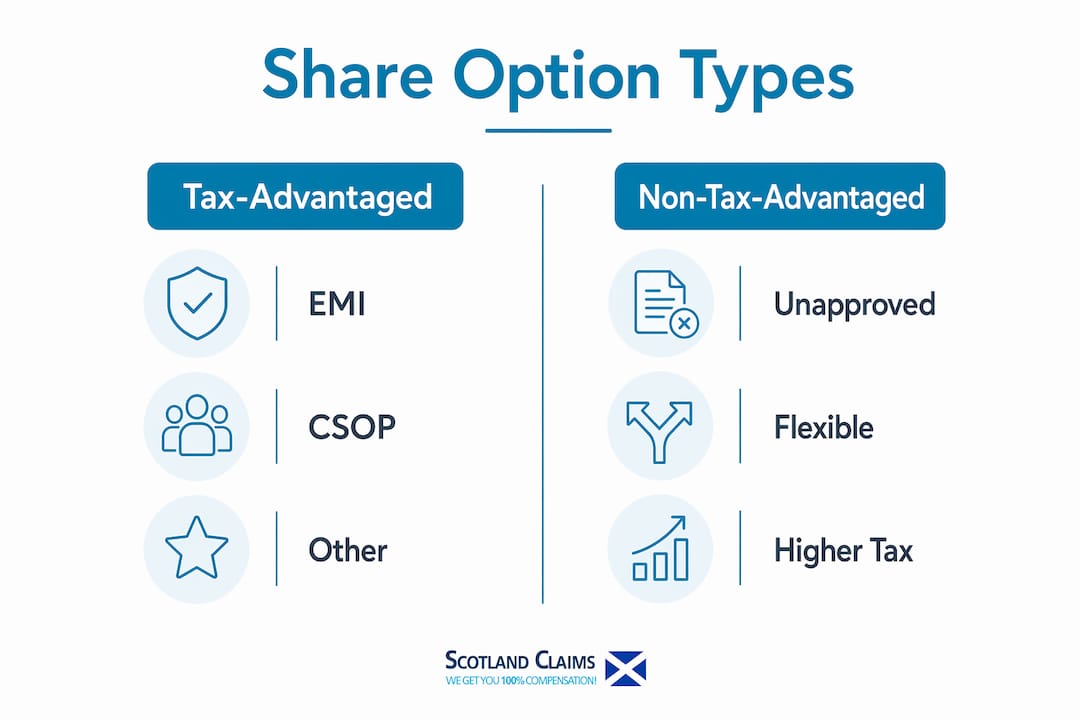

What types of share options exist?

The UK offers several distinct categories of share option scheme. The most important distinction is between tax-advantaged and non-tax-advantaged schemes.

Tax-advantaged schemes

Enterprise Management Incentives (EMI) is the most flexible and tax-efficient option for smaller companies. Following 2026 changes, EMI qualifying thresholds now allow companies to grant options up to £6 million company-wide and £250,000 per employee, with exercise periods extended to 15 years and employee headcount eligibility raised to 500. That expansion makes EMI accessible to a wider range of Scottish businesses than before.

Company Share Option Plan (CSOP) suits larger companies that do not qualify for EMI. CSOP allows employees to hold options over shares worth up to £60,000 at the grant date. Like EMI, CSOP options carry no income tax or National Insurance on exercise when conditions are met.

Non-tax-advantaged schemes

Non-tax-advantaged options, sometimes called unapproved options, carry no HMRC approval. They offer more flexibility in terms of who can receive them and how they are structured, but the tax treatment is significantly less favourable. Income tax and National Insurance apply on exercise, based on the difference between the exercise price and the market value at that point.

| Scheme type |

Tax on grant |

Tax on exercise |

Exercise period |

| EMI |

None |

None (if qualifying) |

Up to 15 years |

| CSOP |

None |

None (if qualifying) |

3–10 years |

| Unapproved |

None |

Income tax and NI |

Flexible |

Pro Tip: Ask your employer or HR team to confirm in writing whether your options are granted under a tax-advantaged scheme. The difference in tax treatment can be worth thousands of pounds over the life of your options.

How do share options work in practice for employees in Scotland?

The lifecycle of a share option follows a clear sequence: grant, vesting, exercise, and sale. Each stage carries distinct rights and obligations.

Grant is when your employer formally awards you the option. You receive a written agreement setting out the number of shares, the exercise price, the vesting schedule, and any conditions attached.

Vesting is the process by which your right to exercise the option becomes active. Most schemes use time-based vesting, typically over three to four years, sometimes with a one-year cliff before any options vest. Performance conditions are also common, particularly in listed companies.

Once vested, you can exercise your options by paying the exercise price and receiving the shares. At this point, option holders gain shareholder rights for the first time, including voting rights and entitlement to dividends.

Key practical points to understand before accepting options:

- Leaver provisions determine what happens to your options if you leave the company. “Good leavers” (redundancy, ill health) typically retain vested options. “Bad leavers” (resignation, dismissal) may forfeit all options.

- Disqualifying events can strip EMI options of their tax-advantaged status. These include a change of company control or the employee ceasing to meet working time requirements.

- Exercise windows are often restricted. Many schemes only allow exercise during set periods, particularly in private companies ahead of a sale or fundraising event.

- Vesting conditions must be met in full. Failing a performance target can result in partial or total lapse of options.

Understanding your employment rights in Scotland is useful context when reviewing the terms of any share option agreement, particularly around leaver provisions and contractual obligations.

Pro Tip: Read your scheme rules document before signing. Pay particular attention to the leaver provisions and any performance conditions. These two clauses determine whether your options are worth anything if circumstances change.

What are the tax implications of share options for Scottish employees?

Tax treatment is where share options become genuinely complex, and where Scottish employees face a distinct position compared to the rest of the UK.

Tax-advantaged options

EMI and CSOP options carry no income tax or National Insurance on grant or exercise, provided qualifying conditions are met. This is a substantial benefit. EMI options deliver up to 29% tax savings compared to non-tax-advantaged options. That saving reflects the avoidance of income tax and National Insurance that would otherwise apply on exercise.

When you sell shares acquired through EMI, Capital Gains Tax (CGT) applies on any gain above your annual exempt amount. From april 2026, Business Asset Disposal Relief applies at 18%, which remains lower than the standard CGT rates for higher-rate taxpayers.

Non-tax-advantaged options

Unapproved options trigger income tax and National Insurance on exercise. The taxable amount is the difference between the exercise price and the market value of the shares on the exercise date. In Scotland, this gain is subject to income tax at your marginal rate.

Scottish income tax rates in 2026 reach 48% for the highest earners. That means an employee exercising options on shares worth £50,000 above the exercise price could face a tax bill of up to £24,000 before any employer sell-to-cover arrangement is in place.

| Tax event |

EMI |

CSOP |

Unapproved |

| On grant |

No tax |

No tax |

No tax |

| On exercise |

No income tax or NI |

No income tax or NI |

Income tax and NI on gain |

| On sale |

CGT on gain |

CGT on gain |

CGT on gain |

Pro Tip: Confirm your scheme classification with your employer before exercising any options. If your options are unapproved, plan for the tax liability in advance. A sell-to-cover arrangement, where some shares are sold immediately to fund the tax bill, can prevent a cash shortfall.

What practical steps should employees know before exercising options?

Exercising share options is not simply a matter of deciding to buy. Several procedural and compliance steps apply, and missing them can be costly.

-

Check your vesting schedule. Confirm exactly how many options have vested and whether any performance conditions remain outstanding. Your scheme administrator or HR team holds this information.

-

Obtain a current share valuation. For private companies, the market value of shares is not publicly listed. Your employer should provide a valuation, often agreed with HMRC under a Share Valuation arrangement.

-

Calculate your tax position before exercising. For unapproved options, the tax liability arises on the exercise date, not the sale date. You need to know the gain before you commit.

-

Understand your employer’s reporting obligations. Employers must report share option grants and exercises to HMRC annually. The filing deadline for the 2025/26 tax year is 6 july 2026. Missing this deadline triggers penalties and can affect your personal tax position.

-

Consider the sell-to-cover option. If your employer offers a sell-to-cover arrangement, you can sell a portion of your newly acquired shares immediately to fund the income tax and National Insurance due. This avoids the need to fund the tax bill from other savings.

-

Review post-exercise restrictions. Some schemes impose lock-up periods after exercise, preventing you from selling shares immediately. This creates a risk if the share price falls between exercise and sale.

Meeting compliance requirements around share option reporting is the employer’s responsibility, but understanding the timeline protects your own tax position and avoids unwelcome surprises.

Key takeaways

Share options are contractual rights to buy shares at a fixed price, and the scheme type determines almost everything about their tax efficiency and practical value.

| Point |

Details |

| Options are not immediate ownership |

You gain no shareholder rights until you exercise and pay the exercise price. |

| Scheme type drives tax outcome |

EMI and CSOP options avoid income tax on exercise; unapproved options do not. |

| Scottish rates amplify the difference |

Marginal income tax rates up to 48% in Scotland make scheme classification critical. |

| Vesting conditions must be met |

Failing performance targets or leaving as a “bad leaver” can result in total loss of options. |

| Employer reporting deadlines matter |

HMRC requires annual reporting by 6 july 2026 for the 2025/26 tax year; penalties apply for late filing. |

Why most employees accept options without reading the small print

Share options are genuinely valuable. I have seen employees in Scottish growth companies build meaningful wealth through well-structured EMI schemes, particularly where the company later sold or listed. The tax efficiency of EMI is real. Aligning personal incentives with company performance works, especially in businesses where cash salaries are constrained.

The problem is that most employees accept options without reading the scheme rules. They focus on the headline number of shares and the exercise price, and ignore the leaver provisions, the vesting conditions, and the tax classification. I have spoken to people who discovered their options were unapproved only when they received a tax bill on exercise. That is an avoidable situation.

Many employees underestimate tax liabilities under unapproved schemes, and in Scotland the consequences are sharper than elsewhere in the UK because of higher marginal rates. The 48% top rate is not theoretical for many professionals in Edinburgh or Glasgow.

My advice is straightforward. Before you accept any share option grant, ask three questions: Is this scheme tax-advantaged? What happens to my options if I leave? When and how can I exercise? If you cannot get clear answers in writing, treat the options as speculative rather than guaranteed value. Consulting a financial adviser or employment law specialist before exercising a large option grant is money well spent.

— Roger

How Scotland Claims Injury Lawyers can help if workplace issues affect you

Share options are tied to your employment, and workplace disputes or injuries can affect your ability to meet vesting conditions or exercise your rights. If you have suffered a workplace injury in Scotland, Scotland Claims Injury Lawyers works on a No Win No Fee basis, meaning you pay nothing upfront and keep 100% of your compensation. Other firms typically deduct a success fee of up to 20% from your settlement. Scotland Claims Injury Lawyers takes nothing from your payout. Whether you have been injured in a road traffic accident, a slip or trip, or a workplace accident, you can speak to specialist injury lawyers in Scotland or use the no win no fee service to understand your options at no cost.

FAQ

What are share options in simple terms?

A share option is a contractual right to buy a set number of company shares at a fixed price on a future date. You are not obliged to buy, and you pay nothing until you choose to exercise the option.

Do share options count as income in Scotland?

Tax-advantaged options such as EMI and CSOP do not trigger income tax on exercise. Non-tax-advantaged options do, with the gain taxed at your marginal rate, which reaches up to 48% in Scotland for higher earners.

What happens to my share options if I leave my employer?

Your outcome depends on whether you are classified as a “good leaver” or “bad leaver” under your scheme rules. Good leavers typically retain vested options; bad leavers may forfeit all options, including vested ones.

How long do I have to exercise EMI options?

Following 2026 changes, EMI exercise periods extend to 15 years from the date of grant, giving employees significantly more flexibility than under previous rules.

What is the difference between share options and shares?

Shares give you immediate ownership, voting rights, and dividend entitlement. Share options give you the right to buy shares at a future date. You gain no shareholder rights until you exercise the option and complete the purchase.

Recommended